The Time-Value Shift: How HelloFresh is Leading the Ready-To-Eat Market Boom

An Investment Case on the Silent Market Leader You Didn’t Even Know Was HelloFresh

1. Executive Summary

HelloFresh SE, founded in 2011 and headquartered in Berlin, has grown to be a leader in the meal kit industry, operating in numerous countries across Europe, North America, and Australasia. Whilst traditionally known for its meal kits, it is making a strong strategic shift towards the rapidly expanding Online Ready-to-Eat (RTE) market, which is expected to grow to around $70 billion to $90 billion by 2029. This pivot is driven by changing consumer preferences, with a growing demand for convenience, time-saving meal solutions, and healthier eating options. The company’s 2020 acquisition of Factor, a leader in the RTE meal delivery space, has positioned HelloFresh to capitalise on these trends. Factor’s fully prepared, health-focused meals, such as keto and low-carb options, are gaining traction, contributing to the company's impressive growth in the RTE segment.

The RTE market offers vast opportunities, supported by factors such as urbanisation, the rise of dual-income households, and increased time constraints on consumers. This expansion, combined with in-store advertising for HelloFresh’s online offerings, could enhance brand visibility and customer acquisition. As HelloFresh moves into this phase, its focus on RTE, combined with continued innovation in meal kits, positions the company for sustained growth in both categories. In the coming years, I foresee a genuine domination of the online ready-to-eat meals market, with a similar expansion to the likes of Amazon. The focus will be on gaining customers and increasing revenues, with constant reinvestment into the business using free cash flows, with the intention of streamlining their operations once a very dominant market share is solidified. This combination of revenue and margin expansion in the long term is what should drive HelloFresh’s stock price to multiply.

And what’s the most interest part of all? Most people do not even know that HelloFresh are the market leader let alone even operate in the RTE Meals Industry which means that when this becomes common knowledge it could be too late to capture the 10x or more returns that could occur.

2. Company Overview

HelloFresh SE (HFG), together with its subsidiaries, operates as a meal kit provider for the home industry. The company offers premium meals, protein swaps, double portions, and extra recipes, as well as add-ons such as soups, snacks, fruit boxes, desserts, ready-to-eat meals, and seasonal boxes. It has operations in the United States, Canada, Australia, Austria, Belgium, Germany, Denmark, France, Luxembourg, the Netherlands, New Zealand, Switzerland, Sweden, Spain, Norway, Italy, and the UK. The company operates under the HelloFresh brand and owns the following brands:

Chefs Plate – Acquired in 2018, Chefs Plate is a Canadian meal kit service that offers a variety of recipes, including quick-prep meals.

Good Chop – A US-based sustainable meat delivery service offering ethically sourced, high-quality meat.

The Pets Table – Launched by HFG in 2023, marking its entry into the pet food market. This new venture focuses on delivering high-quality, nutritious meals for pets, primarily dogs. The Pets Table offers fresh, tailored meals based on the specific nutritional needs of pets, similar to how HelloFresh designs its meal kits for humans.

Green Chef – Acquired in 2018, Green Chef focuses on organic and special-diet meal kits, including options for keto, paleo, and plant-based lifestyles.

EveryPlate – Launched by HelloFresh in 2018, EveryPlate is a more affordable meal kit option, focusing on simple, budget-friendly recipes and ingredients.

Factor – Acquired in 2020, Factor (formerly Factor75) is a ready-to-eat meal delivery service that provides fully prepared meals catering to health-conscious consumers with options like keto, low-carb, and calorie-smart meals.

Youfoodz – Acquired in 2021, Youfoodz is an Australian meal delivery service offering fresh, ready-made meals, snacks, and drinks.

3. Problem/Solution

Problem

HelloFresh’s initial problem was the inconvenience of shopping for food and learning how to cook home meals from scratch. Their solution was ready-to-cook meal packs with all the ingredients and a simple-to-follow recipe. This was great, although expensive, but this business model has since become outdated due to the unsustainability of demand. I even experienced this myself: my parents used the service, but once we had cooked a meal, we knew what ingredients to buy and how to cook it, so we didn’t need HelloFresh again.

The current problem is different, though. In a world where time is so valuable due to the demands of work, social life, family, and more, cooking is often at the bottom of people’s to-do lists. There is a market of consumers willing to pay for this cooking to be done, but not in the form of fast food—people still want high-quality, nutritious meals.

Solution

HelloFresh’s solution? Ready-to-Eat (RTE) meals. Meal kits are staying, but RTE meals, through the Factor75 brand, are now their main focus due to changing consumer demands. They acquired Factor in 2020 and have shifted the majority of their focus to this for future growth. Why is their service needed? As explained above, people want to be able to do more with their lives due to the growing number of activities available, such as travelling, sports, etc., along with an accelerated transition to healthier living and a more balanced lifestyle with work and family. How do people achieve these goals? Time.

Time is the most valuable asset for many people, and spending time cooking, unless it is an enjoyable hobby, is one of the many factors that reduce the time available for other pursuits. Not only this, but people want to ensure they are staying healthier than we have generally been as a population in recent decades. This trend has been accelerated by the COVID-19 pandemic, as more people have adopted healthier lifestyles. So, what is HelloFresh’s solution to both of these consumer trends? Factor75. Ready-to-eat meals that are high-quality and nutritious, saving consumers time on cooking while providing excellent nutritional value. These meals offer not only increased convenience but also portability, which is essential for the growing ‘on-the-go’ lifestyle that many now lead.

This is the main market I will be focusing on in this write-up; however, HelloFresh also operates multiple other brands, which will be “extras” to the overall thesis and valuation of the company.

4. Market Analysis

The main market we need to focus on predominantly is the Ready-To-Eat (RTE) Meal Kit Delivery Market. However, I will also be looking at the Heat-and-Eat Market and the Meal Kit Delivery Service Market. The formal definitions for these markets from Statista are below:

“The eCommerce Ready-to-Eat Meals market refers to the online platform where consumers can purchase pre-prepared meals that are ready to eat. These meals are typically prepared by professional chefs or culinary experts and are delivered directly to the consumers' doorstep. The eCommerce platform provides a convenient and time-saving solution for individuals who are looking for quick and easy meal options without the need for cooking or meal preparation.”

“The Ready-to-Eat Meals market covers prepared food and meals that can be eaten as is or after minimal preparation. These meals do not require cooking and are typically consumed after heating. These meals may also include disposable eating utensils. Classic frozen foods include meat, fish, vegetables, filled pasta, and frozen pizzas.”

“Meal kits are pre-packaged boxes of ingredients and recipes that are delivered to customers' homes. Each kit includes all the ingredients needed to make a specific meal, along with step-by-step instructions for preparing the dish. The idea behind meal kits is to make it easy for people to cook delicious, healthy meals at home without having to plan and shop for ingredients themselves. Many meal kit companies offer a range of dishes to choose from, and some also offer options for specific dietary needs, such as vegetarian or gluten-free meals.”

As usual, there are various market research papers on these industries, and I have taken estimates for current and future sizes based on the multiple research reports that give slightly different figures. Statista was my main source for these reports.

Market Opportunity

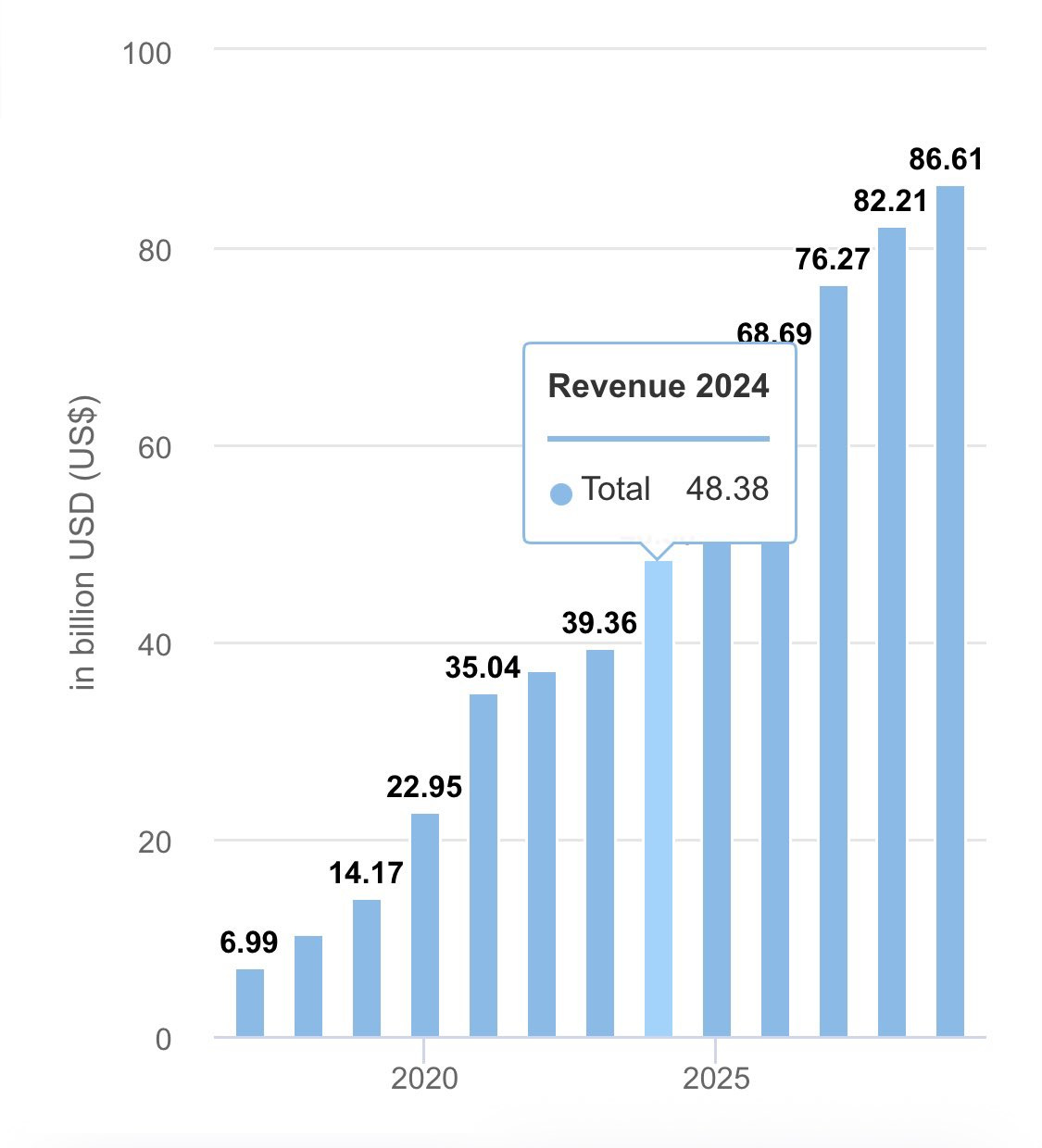

2024 Market Size

Online RTE Market: $50 billion

RTE Market: $600 billion

Meal Kit Delivery Market: $13 billion

2029 Market Projection

Online RTE Market: $85 billion (12% CAGR)

RTE Market: $800 billion (6.5% CAGR)

Meal Kit Delivery Market: $16.5 billion (4.5% CAGR)

Main Sources (Others Considered)

Ready-to-Eat Meal eCommerce Market Worldwide - Statista

The market that HelloFresh is now predominantly working in is the Online RTE Market, which is expected to grow to around $70bn–$90bn by 2029.

Main Drivers of this Market

Shifts towards healthier lifestyles

Urbanisation trends

Increased demands on people's time

Prioritisation of convenience

Prevalence of dual-income households

Changing lifestyle demands

On top of the above, there is the added opportunity of the meal kit service market, along with the RTE Market, which includes frozen and refrigerated meals sold in stores. HelloFresh could target this market with premium RTE meals aimed at higher-net-worth consumers. My view is that by having products in more upmarket stores, with packaging that advertises the online delivery service, HelloFresh could build out its customer base further. This would allow the company to capture in-store sales (which are unlikely to be extraordinary in volume) but would provide the major benefit of increased brand awareness for its offerings.

5. Competitors

Main Competitors:

Home Chef → Acquired by Kroger in 2018 for $200 million + $500 million in potential add-ons.

Blue Apron → Bought out by Wonder for $103 million in November 2023 after declining revenues since 2018.

Sunbasket

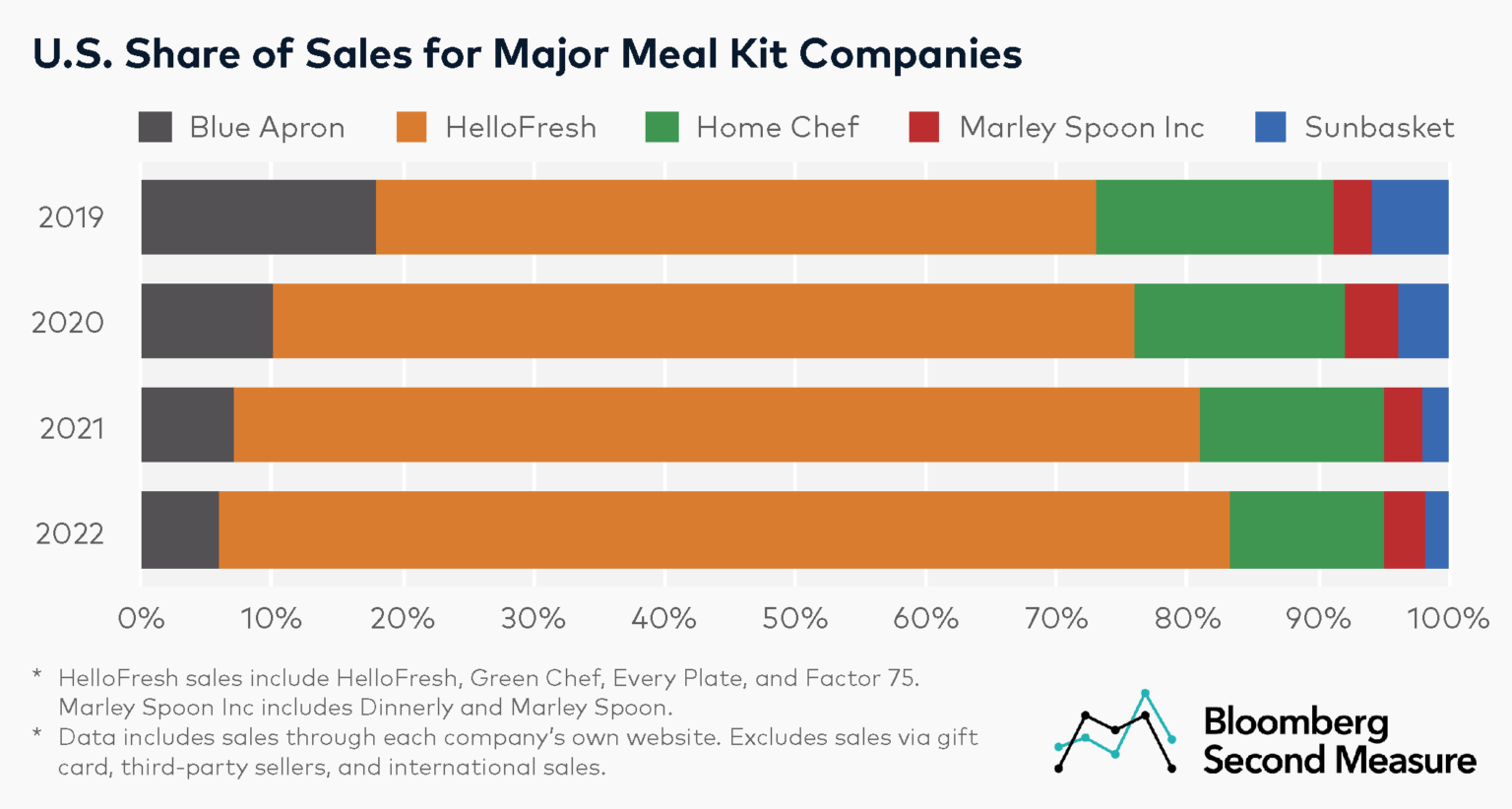

Home Chef is by far their largest competitor, acquired by Kroger in 2018 for $200 million, with a potential $500 million in add-ons depending on KPIs being hit over the following five years. A quick overview of their offerings is below:

Dinner: A selection of traditional dinner recipes designed for family meals, featuring a variety of proteins and sides.

Express: Quick and easy meals that can be prepared in 30 minutes or less, perfect for busy weeknights.

Oven-Ready: Meals that come pre-prepped and can be cooked directly in the oven, offering convenience without sacrificing flavour.

Lunch: Options designed for midday meals, typically lighter and easy to pack for work or school.

Extras: Small snacks and extras such as waffles, bread rolls, muffins, etc. This includes Breakfast, Snacks, Desserts, Salads, Protein, and Beverages.

They have roughly 35+ meals and 19+ extras available each week, and the menu changes on a weekly basis. The website is clean, the branding is excellent, and they have grown extensively. The most up-to-date figures over an 8-year period to 2021 show that they went from bootstrapping funding to $1 billion in sales, which is impressive. Looking at the market share split for meal kit services (there is not enough data on the RTE market yet), we can see that Home Chef’s growth, although impressive, could also be attributed to the overall market gaining traction, especially during COVID:

Who was the only company notably gaining market share? HelloFresh.

6. Company Analysis

The main focus of this analysis will be on Factor75, HelloFresh’s Ready-To-Eat Meal Service, which many people seem to be unaware of. The common perception of HelloFresh is as a meal kit company, and while their kits are often seen as expensive, the company has changed. We could be reaching an inflection point where this change starts to become more widely recognised by investors. Looking at HelloFresh’s H1 2024 update, we can see the management board’s perspective on this transition, and they seem extremely confident about a long-term shift. The tone suggests we may soon reach a point where more investors notice these changes.

Future Outlook & Past Accountability

Meal Kits

Meal kits have been and remain their “largest and most profitable product category.” The success of meal kits over the last 12 years has allowed HelloFresh to “generate significant amounts of free cash flow,” which has funded their “state-of-the-art fulfilment network, new verticals, and a global expansion strategy for meal kits and now RTE meals.” However, revenue and margins in the meal kit space have fallen recently, becoming “the biggest drag on financial performance.” Due to the demand surge during the pandemic, they were “overly optimistic in forecasting future top-line growth,” resulting in a cost base that is now too high.

Increasing Efficiency

They have been aware of these issues for some time and have taken steps to address the challenges by “streamlining capacity, re-examining capital expenditure plans, leveraging fulfilment centres with the latest technology and automation capabilities, and shedding other costs.”

Continued Innovation

Despite this, they remain committed to innovating for customers, especially in the meal kit space, where they have reduced cooking times and tripled their weekly recipe options over the past three years. They are also integrating RTE meal assortments with meal kits to provide consumers with a broader range of choices.

Ready-To-Eat Meals

In the Ready-To-Eat meal service, the management board sees “strong growth tailwinds,” with expectations that by 2029 their “RTE product category will be both larger and more profitable than the entire group was before the pandemic.” Key growth drivers include:

Penetrating the still early-stage North American market

International expansion

Accessing new customer groups

Offering differentiated price tiers

Expanding distribution channels

They also believe that Factor is still at a significantly lower brand awareness level compared to HelloFresh in the US, reinforcing the view that the brand has already gone through the difficult stages of transition and is showing exceptional growth, with many more tailwinds ahead.

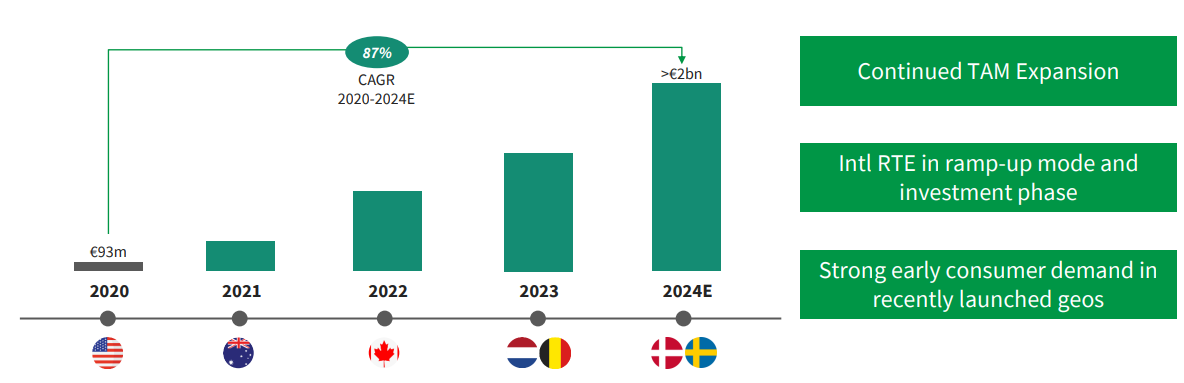

Domestic and International Expansion

Global expansion has already begun, with several countries being targeted, as shown in the Q1 2024 earnings report:

In addition to the above, they have plans to target other markets for the remainder of 2024 and into 2025. Since the expansion into other countries has already been so successful, they feel confident enough to continue expanding before focusing on specific countries. My main takeaway from this is that they are keen to build an early presence in as many locations as possible. Being the market leader in this segment, with a superior brand and the capabilities to expand, they do not want to miss out on the early-mover advantage in any location, as they see potential growth in the future. In their words from other annual reports, they are “doubling down” on the RTE market by leveraging their current resources. They are maintaining their other businesses and brand awareness but focusing on the significant opportunity in RTE meals with their Factor brand (YouFoodz in Australia & Chef’s Plate in Canada).

“We are confident that the RTE product category will not just be a growth story but also one of margin expansion in the coming years. This will be driven in the near term by the scale of our Arizona facility, and in the mid-term, by the maturing of the customer base and the subsequent reduction in marketing spend as a percentage of revenue.” We are about to see mega-revenue expansion combined with long-term margin improvements, which they expect to reach the “same margin level as the meal-kit segment at the very least, given that the per-customer unit economics looks at least as attractive as meal kits.”

And how about the long-term outlook? They want to “change the way people eat forever” and see two main trends:

Clear consumer appetite for “digital-first” approaches to meal times at home.

HFG has built a clear and growing market position in each of the multi-billion dollar categories they operate/have operated in, despite competition from VC start-ups, e-commerce giants, traditional FMCG (fast-moving consumer goods) companies, and big grocers.

The focus now is on “efficiency and meaningfully expanding free cash flows and profitability of the Group." Why do I highlight “Group”? They are streamlining ALL of their business. At €7.5 billion in annual revenue, with a market cap of €1.4 billion...

My Main Takeaways from the Above

What I see is a company that has identified a genuine paradigm shift in consumer behavior. This shift is not as revolutionary as AI, but it is potentially a radical change where consumers are prioritizing time and convenience over the money saved from traditional shopping and cooking habits. They have clearly stated their intent to “double down” on this segment with their RTE meals. The CEO has underscored this commitment with a €10 million share purchase of HFG stock this summer, his first since 2020. As I often note, when management and employees repurchase stock, it is generally a good sign—especially when the company has struggled and many executives might otherwise be inclined to "jump ship."

What we are potentially about to see is huge revenue expansion in a more profitable segment, which will translate into increased profits with improved efficiency and economies of scale over time.

Key Data Points

I will quickly run through some of the key financial data and multiples for HelloFresh before moving on to concluding thoughts and some potential price targets:

Summarised Factor Brand Growth

87% Revenue CAGR over 4 years, with revenues increasing from €93m in 2020 to over €2 billion expected this year.

2023 YoY Revenue Growth: 60.0%

Q1 2024 YoY Revenue Growth: 56.0%

Q2 2024 YoY Revenue Growth: 45.2%

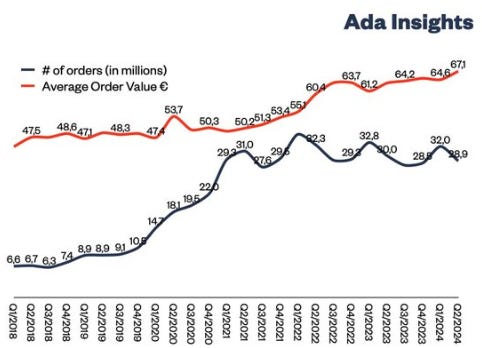

Revenue increased YoY in H1 2024 from €3.93 billion in H1 2023 to €4.02 billion in H1 2024 (+2.3%), primarily driven by a 5.5% increase in the Average Order Value (AOV) to €65.8, partially offset by a 3.1% decrease in the number of orders. This can be attributed to a slowing demand for meal kits, which represent the “legacy” business and are no longer the core focus. They are now leveraging resources and experience from this market into the RTE market, giving them an even higher competitive advantage.

ADA Insights, Average Order Value vs # of Online Orders

Contribution Margin (excluding share-based compensation) decreased as a percentage of revenue from 27.4% in H1 2023 to 24.7% in H1 2024. This increase in variable costs is mainly due to procurement and cooking expenses, which increased from 34.9% of revenue in H1 2023 to 37.4% in H1 2024. The higher share of RTE meals requires higher production costs. However, fulfillment expenses are lower for this segment due to improving efficiency in logistics and packaging operations.

Marketing Expenses increased as a percentage of revenue by 1.7%, from 18.4% in H1 2023 to 20.1% in H1 2024, as they aggressively build out the Factor brand. However, marketing expenses as a percentage of revenue were actually down YoY in Q2 2024.

General and Administrative Expenses were down YoY from 5.5% in H1 2023 to 5.3% in H1 2024, illustrating a greater focus on cost discipline at HelloFresh.

H1 2024 Cash & Cash Equivalents: €433m vs €504m H1 2023

H1 2024 Net Cash Flow: €147m vs €207m H1 2023

Net Assets: €954m vs €1,019m Dec 31, 2023 (~€14/share vs €8.50 today)

The reason HelloFresh is currently losing money (though they are expected to turn a small profit this year) is that, like Hims and Hers Health, they are reinvesting most of their capital back into the business to aggressively expand operations. This is reminiscent of Amazon's early story, where there was no immediate incentive for turning net income profits. Instead, HelloFresh aims to maximize future revenues by building out the largest RTE meal business in the world and capturing as much of the $85 billion market by 2029 as possible. Once this is achieved, there will be a greater focus on increasing profitability.

Besides the points mentioned about the RTE segment, there are other areas of the business that could contribute to future growth. I will explore these another time. However, for now, the RTE segment is the main driver of future growth and is the primary focus.

7. Concluding Thoughts

I believe the market is unaware of the inflection point HelloFresh has reached, and the paradigm shift in consumer behavior toward cooking and shopping for food. This shift will continue to accelerate. HelloFresh does not face competition that can match them in size or scalability. Furthermore, they are transitioning from being a “non-essential” producer to an “acute pain solver,” addressing the consumer demand for convenience. With consistently strong cash flows from operations and lower capital expenditure, I expect HelloFresh to continue expanding their RTE segment rapidly, dominating the market in the short, mid, and long term, and reaping the benefits through substantial profits in the future.

Projecting price targets and future earnings is tricky, given the company’s current trajectory. Instead, I will outline a potential revenue growth scenario and how this could look with different future EBITDA margins, which management expects to reach at least the same level as their meal kit service (which has hovered around 10%–15%).

Revenue Growth Forecast

2021: €275 million (+195.7%)

2022: €875 million (+218.18%)

2023: €1.4 billion (+60.0%)

2024: €2.0 billion (+42.86%)

2025: €2.9 billion (+45.0%)

2026: €4.06 billion (+40.0%)

2027: €5.52 billion (+36.0%)

2028: €7.29 billion (+32.0%)

2029: €9.48 billion (+30.0%)

This growth may seem aggressive for a €1.4 billion company, but how does it look as a share of the total worldwide market up to 2029?

2024: 4.1%

2025: 5.1%

2026: 5.9%

2027: 7.2%

2028: 8.9%

2029: 10.9%

It is clear that HelloFresh is a market leader in the meal kit industry and is beginning to dominate the RTE meal industry. Who's to say they cannot capture even more market share by 2029? If they do, revenues will be even higher. Now, if we apply EBITDA margins of 10%, 12.5%, 15%, and 17.5%, we get the following:

2029 EBITDA Margins (Factor only)

10%: €947.5 million

12.5%: €1.18 billion

15%: €1.42 billion

17.5%: €1.66 billion

A 17.5% margin is likely unreasonable, given that the focus in the next few years will be on expansion. Margin improvements will probably come down the line as expansion foundations are laid. However, a 10% margin by 2029 is not unreasonable, as they sit at ~4% currently, with the possibility of increasing margins closer to 15% over time as the business matures.

I will not be giving price targets for HelloFresh at this current moment, however I genuinely think this is an opportunity potentially worth multiples of what it is currently trading for and the market will be very surprised with what is to come over the years.

Thanks for this excellent write-up. I am an owner myself, did not quite catch the falling knife but already at a nice profit following the rocket boost that CEO's $10m purchase on the open market generated. Fully agree that meal kits are becoming outdated and that the future is RTE, while the market price does not reflect RTE's growth at all - market is still treating Hellofresh as a fad that's about to disappear completely.

By the way, one really funny aspect of investing in Hellofresh in the micro / small cap space is that almost everyone is bearish because in my experience microcap investors are a bit like the early Warren Buffett was with respect to money management. They would not buy a coffee for $4, much less a $15 RTE meal, if they can make one at home for next to nothing, and they tend to regard Hellofresh through this same heavily biased prism. I am sure you would get much more bullish on Hellofresh if you talked to, say, lawyers, doctors, you name it, who literally couldn't be bothered about saving a few hundred bucks a month on groceries if it buys them one more hour of free time a day.